Page 316 - F1 Integrated Workbook STUDENT 2018

P. 316

Chapter 19

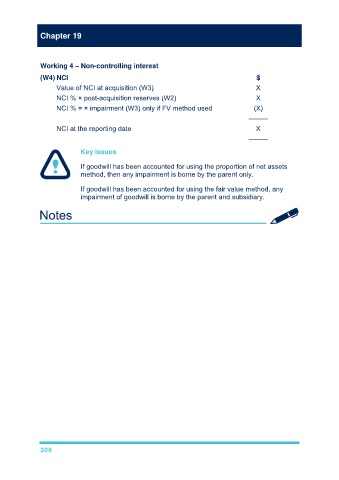

Working 4 – Non-controlling interest

(W4) NCI $

Value of NCI at acquisition (W3) X

NCI % × post-acquisition reserves (W2) X

NCI % = × impairment (W3) only if FV method used (X)

–––––

NCI at the reporting date X

–––––

Key issues

If goodwill has been accounted for using the proportion of net assets

method, then any impairment is borne by the parent only.

If goodwill has been accounted for using the fair value method, any

impairment of goodwill is borne by the parent and subsidiary.

306