Page 333 - F1 Integrated Workbook STUDENT 2018

P. 333

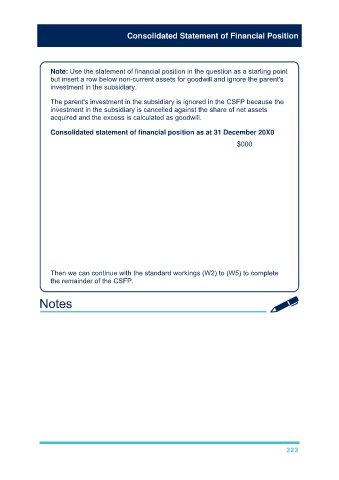

Consolidated Statement of Financial Position

Note: Use the statement of financial position in the question as a starting point

but insert a row below non-current assets for goodwill and ignore the parent's

investment in the subsidiary.

The parent's investment in the subsidiary is ignored in the CSFP because the

investment in the subsidiary is cancelled against the share of net assets

acquired and the excess is calculated as goodwill.

Consolidated statement of financial position as at 31 December 20X0

$000

Non-current assets

Goodwill (W3)

Property, plant and equipment (3,330 + 550) 3,880

Current assets (1,030 + 660) 1,690

––––

––––

Equity

Share capital 2,500

Retained earnings (W5)

Non-controlling interest (W4)

Current liabilities (400 + 100) 500

––––

––––

Then we can continue with the standard workings (W2) to (W5) to complete

the remainder of the CSFP.

323