Page 68 - FINAL CFA I SLIDES JUNE 2019 DAY 3

P. 68

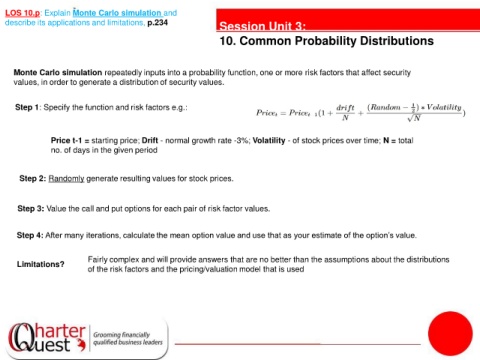

LOS 10.p: Explain Monte Carlo simulation and

describe its applications and limitations, p.234 Session Unit 3:

10. Common Probability Distributions

Monte Carlo simulation repeatedly inputs into a probability function, one or more risk factors that affect security

values, in order to generate a distribution of security values.

Step 1: Specify the function and risk factors e.g.:

Price t-1 = starting price; Drift - normal growth rate -3%; Volatility - of stock prices over time; N = total

no. of days in the given period

Step 2: Randomly generate resulting values for stock prices.

Step 3: Value the call and put options for each pair of risk factor values.

Step 4: After many iterations, calculate the mean option value and use that as your estimate of the option’s value.

Fairly complex and will provide answers that are no better than the assumptions about the distributions

Limitations?

of the risk factors and the pricing/valuation model that is used