Page 345 - Microsoft Word - 00 BA3 IW Prelims STUDENT.docx

P. 345

Answers to questions

Example 5: Solution (cont.)

The part of the statement of profit or loss which calculates gross profit is known

as the trading account. The trading account is thus a sub-section of the statement

of profit or loss although its name does not appear within the statement of profit or

loss. Nevertheless, it is a very important in your exam part of the statement of

profit or loss and you may be asked to prepare a trading account.

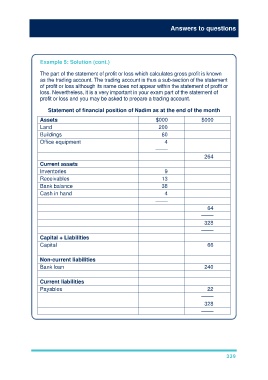

Statement of financial position of Nadim as at the end of the month

Assets $000 $000

Land 200

Buildings 60

Office equipment 4

––––

264

Current assets

Inventories 9

Receivables 13

Bank balance 38

Cash in hand 4

––––

64

––––

328

––––

Capital + Liabilities

Capital 66

Non-current liabilities

Bank loan 240

Current liabilities

Payables 22

––––

328

––––

339