Page 414 - Microsoft Word - 00 BA3 IW Prelims STUDENT.docx

P. 414

Chapter 20

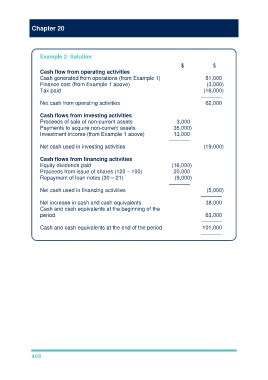

Example 2: Solution

$ $

Cash flow from operating activities

Cash generated from operations (from Example 1) 81,000

Finance cost (from Example 1 above) (3,000)

Tax paid (16,000)

–––––––

Net cash from operating activities 62,000

Cash flows from investing activities

Proceeds of sale of non-current assets 3,000

Payments to acquire non-current assets 35,000)

Investment income (from Example 1 above) 13,000

–––––––

Net cash used in investing activities (19,000)

Cash flows from financing activities

Equity dividends paid (16,000)

Proceeds from issue of shares (120 – 100) 20,000

Repayment of loan notes (30 – 21) (9,000)

–––––––

Net cash used in financing activities (5,000)

–––––––

Net increase in cash and cash equivalents 38,000

Cash and cash equivalents at the beginning of the

period 63,000

–––––––

Cash and cash equivalents at the end of the period 101,000

–––––––

408