Page 86 - Microsoft Word - 00 BA3 IW Prelims STUDENT.docx

P. 86

Chapter 4

Illustration 1

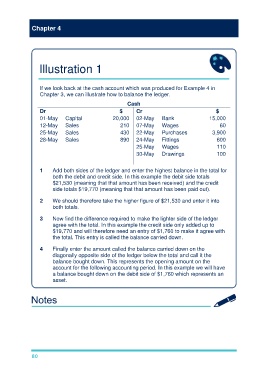

If we look back at the cash account which was produced for Example 4 in

Chapter 3, we can illustrate how to balance the ledger.

Cash

Dr $ Cr $

01-May Capital 20,000 02-May Bank 15,000

12-May Sales 210 07-May Wages 60

25-May Sales 430 22-May Purchases 3,900

28-May Sales 890 24-May Fittings 600

25-May Wages 110

30-May Drawings 100

1 Add both sides of the ledger and enter the highest balance in the total for

both the debit and credit side. In this example the debit side totals

$21,530 (meaning that that amount has been received) and the credit

side totals $19,770 (meaning that that amount has been paid out).

2 We should therefore take the higher figure of $21,530 and enter it into

both totals.

3 Now find the difference required to make the lighter side of the ledger

agree with the total. In this example the credit side only added up to

$19,770 and will therefore need an entry of $1,760 to make it agree with

the total. This entry is called the balance carried down.

4 Finally enter the amount called the balance carried down on the

diagonally opposite side of the ledger below the total and call it the

balance bought down. This represents the opening amount on the

account for the following accounting period. In this example we will have

a balance bought down on the debit side of $1,760 which represents an

asset.

80