Page 10 - PowerPoint Presentation

P. 10

LOS 7.d: Distinguish between the dependent and MODULE 7.2: LINEAR REGRESSION: INTRODUCTION

independent variables in a linear regression.

In a general form straight line equation: Y = a + bX, Y is the Dependent variable (also called the explained, endogenous, or the predicted

variable) and X is the Independent variable (also called the explanatory variable, exogenous, or predicting variable).

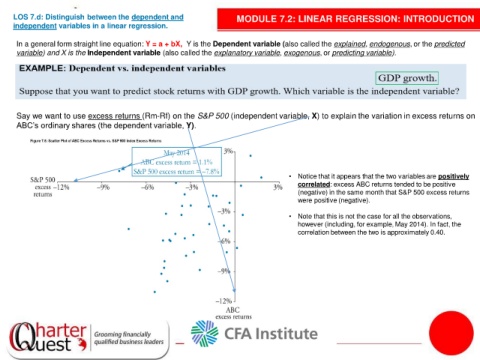

Say we want to use excess returns (Rm-Rf) on the S&P 500 (independent variable, X) to explain the variation in excess returns on

ABC’s ordinary shares (the dependent variable, Y).

• Notice that it appears that the two variables are positively

correlated: excess ABC returns tended to be positive

(negative) in the same month that S&P 500 excess returns

were positive (negative).

• Note that this is not the case for all the observations,

however (including, for example, May 2014). In fact, the

correlation between the two is approximately 0.40.