Page 72 - MAC4861_2 Costing class slides part 2

P. 72

DECISION MAKING

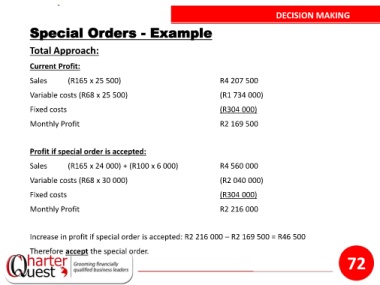

Special Orders - Example

Total Approach:

Current Profit:

Sales (R165 x 25 500) R4 207 500

Variable costs (R68 x 25 500) (R1 734 000)

Fixed costs (R304 000)

Monthly Profit R2 169 500

Profit if special order is accepted:

Sales (R165 x 24 000) + (R100 x 6 000) R4 560 000

Variable costs (R68 x 30 000) (R2 040 000)

Fixed costs (R304 000)

Monthly Profit R2 216 000

Increase in profit if special order is accepted: R2 216 000 – R2 169 500 = R46 500

Therefore accept the special order.

72