Page 31 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 31

The modern business environment

Throughput accounting and the

Theory of constraints

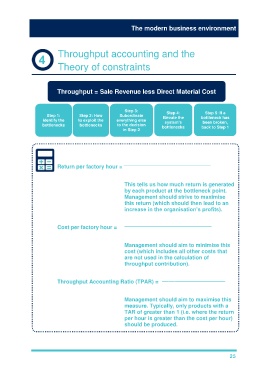

Throughput = Sale Revenue less Direct Material Cost

Step 3: Step 4: Step 5: If a

Step 1: Step 2: How Subordinate

identify the to exploit the everything else Elevate the bottleneck has

system’s

been broken,

bottlenecks bottlenecks to the decision bottlenecks back to Step 1

in Step 2

Throughput per unit

Return per factory hour = –––––––––––––––––––––––––––––

Product time on bottleneck resource

This tells us how much return is generated

by each product at the bottleneck point.

Management should strive to maximise

this return (which should then lead to an

increase in the organisation’s profits).

Total factory costs

Cost per factory hour = –––––––––––––––––––––––––––––

Product time on bottleneck resource

Management should aim to minimise this

cost (which includes all other costs that

are not used in the calculation of

throughput contribution).

Return per factory hour

Throughput Accounting Ratio (TPAR) = –––––––––––––––––––––

Cost per factory hour

Management should aim to maximise this

measure. Typically, only products with a

TAR of greater than 1 (i.e. where the return

per hour is greater than the cost per hour)

should be produced.

25