Page 42 - QEB_2_2016_lowres

P. 42

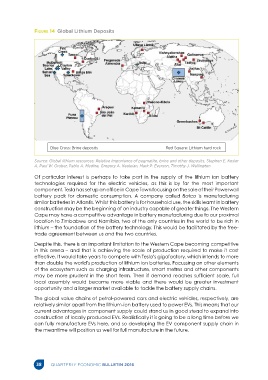

Figure 14 Global Lithium Deposits

Blue Cross: Brine deposits Red Square: Lithium hard rock

Source: Global lithium resources: Relative importance of pegmatite, brine and other deposits, Stephen E. Kesler

A, Paul W. Gruber, Pablo A. Medina, Gregory A. Keoleian, Mark P. Everson, Timothy J. Wallington

Of particular interest is perhaps to take part in the supply of the lithium ion battery

technologies required for the electric vehicles, as this is by far the most important

component. Tesla has set up an office in Cape Town focusing on the sale of their Powerwall

battery pack for domestic consumption. A company called Batco is manufacturing

similar batteries in Atlantis. Whilst this battery is for household use, the skills learnt in battery

construction may be the beginning of an industry capable of greater things. The Western

Cape may have a competitive advantage in battery manufacturing due to our proximal

location to Zimbabwe and Namibia, two of the only countries in the world to be rich in

lithium – the foundation of the battery technology. This would be facilitated by the free-

trade agreement between us and the two countries.

Despite this, there is an important limitation to the Western Cape becoming competitive

in this arena – and that is achieving the scale of production required to make it cost

effective. It would take years to compete with Tesla’s gigafactory, which intends to more

than double the world’s production of lithium ion batteries. Focussing on other elements

of the ecosystem such as charging infrastructure, smart metres and other components

may be more prudent in the short term. Then if demand reaches sufficient scale, full

local assembly would become more viable and there would be greater investment

opportunity and a larger market available to tackle the battery supply chains.

The global value chains of petrol-powered cars and electric vehicles, respectively, are

relatively similar apart from the lithium-ion battery used to power EVs. This means that our

current advantages in component supply could stand us in good stead to expand into

construction of locally produced EVs. Realistically it is going to be a long time before we

can fully manufacture EVs here, and so developing the EV component supply chain in

the meantime will position us well for full manufacture in the future.

38 QUARTERLY ECONOMIC BULLETIN 2016