Page 185 - International Marketing

P. 185

NPP

BRILLIANT'S Overseas Market 187

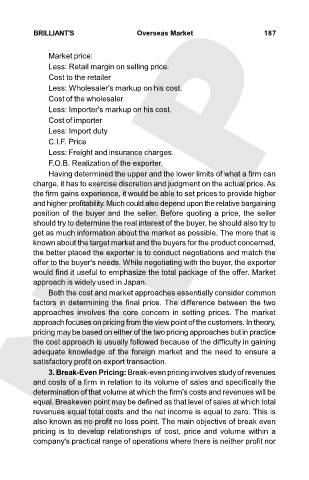

Market price:

Less: Retail margin on selling price.

Cost to the retailer

Less: Wholesaler's markup on his cost.

Cost of the wholesaler

Less: Importer's markup on his cost.

Cost of importer

Less: Import duty

C.I.F. Price

Less: Freight and insurance charges.

F.O.B. Realization of the exporter.

Having determined the upper and the lower limits of what a firm can

charge, it has to exercise discretion and judgment on the actual price. As

the firm gains experience, it would be able to set prices to provide higher

and higher profitability. Much could also depend upon the relative bargaining

position of the buyer and the seller. Before quoting a price, the seller

should try to determine the real interest of the buyer, he should also try to

get as much information about the market as possible. The more that is

known about the target market and the buyers for the product concerned,

the better placed the exporter is to conduct negotiations and match the

offer to the buyer's needs. While negotiating with the buyer, the exporter

would find it useful to emphasize the total package of the offer. Market

approach is widely used in Japan.

Both the cost and market approaches essentially consider common

factors in determining the final price. The difference between the two

approaches involves the core concern in setting prices. The market

approach focuses on pricing from the view point of the customers. In theory,

pricing may be based on either of the two pricing approaches but in practice

the cost approach is usually followed because of the difficulty in gaining

adequate knowledge of the foreign market and the need to ensure a

satisfactory profit on export transaction.

3. Break-Even Pricing: Break-even pricing involves study of revenues

and costs of a firm in relation to its volume of sales and specifically the

determination of that volume at which the firm's costs and revenues will be

equal. Breakeven point may be defined as that level of sales at which total

revenues equal total costs and the net income is equal to zero. This is

also known as no profit no loss point. The main objective of break even

pricing is to develop relationships of cost, price and volume within a

company's practical range of operations where there is neither profit nor