Page 107 - Corporate Finance PDF Final new link

P. 107

NPP

BRILLIANT’S Cash Flow Statement 107

Working Notes:

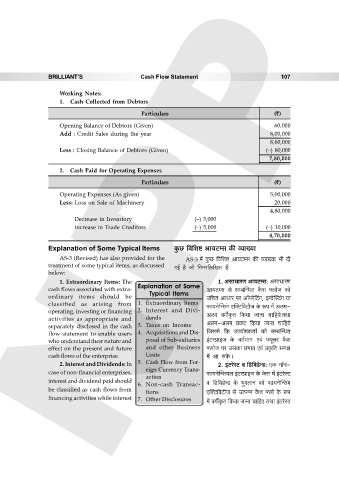

1. Cash Collected from Debtors

Particulars (`)

Opening Balance of Debtors (Given) 60,000

Add : Credit Sales during the year 8,00,000

8,60,000

Less : Closing Balance of Debtors (Given) (–) 80,000

7,80,000

2. Cash Paid for Operating Expenses

Particulars (`)

Operating Expenses (As given) 5,00,000

Less: Loss on Sale of Machinery 20,000

4,80,000

Decrease in Inventory (–) 5,000

Increase in Trade Creditors (–) 5,000 (–) 10,000

4,70,000

Explanation of Some Typical Items Hw$N> {d{eï> Am`Q>åg H$s ì`m»`m

AS-3 (Revised) has also provided for the AS-3 _| Hw$N> {d{eï> Am`Q>åg H$s ì`m»`m ^r Xr

treatment of some typical items, as discussed JB© h¡ Omo {ZåZ{c{IV h¢:

below:

1. Extraordinary Items: The 1. AgmYmaU Am`Q>åg: AgmYmaU

cash flows associated with extra- Explanation of Some Am`Q>åg go gå~pÝYV H¡$e âbmoO H$mo

ordinary items should be Typical Items C{MV AmYma na Am°naoqQ>J, BÝdopñQ>¨J `m

classified as arising from 1. Extraordinary Items \$m`ZopÝg¨J EpŠQ>{dQ>rO Ho$ ê$n _| AcJ-

operating, investing or financing 2. Interest and Divi- AcJ dJuH¥$V {H$`m OmZm Mm{h`oŸVWm

activities as appropriate and dends

separately disclosed in the cash 3. Taxes on Income AcJ-AcJ àH$Q> {H$`m OmZm Mm{h`o

flow statement to enable users 4. Acquisitions and Dis- {Oggo {H$ Cn`moJH$Vm© H$mo gå~pÝYV

who understand their nature and posal of Sub-sidiaries B§Q>aàmBO Ho$ dV©_mZ Ed§ â`yMa H¡$e

effect on the present and future and other Business âbmoO na CgH$m à^md Ed§ àH¥${V g_P

cash flows of the enterprise. Units _| Am gHo$Ÿ&

2. Interest and Dividends: In 5. Cash Flow from For- 2. B§Q>aoñQ> d {S>{dS>oÝS>: EH$ Zm°Z-

eign Currency Trans-

case of non-financial enterprises, \$m`ZopÝe`b B§Q>aàmBO Ho$ Ho$g _| B§Q>aoñQ>

action

interest and dividend paid should d {S>{dS>oÝS> Ho$ ^wJVmZ H$mo \$m`ZopÝg¨J

6. Non-cash Transac-

be classified as cash flows from

tions EpŠQ>{dQ>rO go CËnÝZ H¡$e âbmo Ho$ ê$n

financing activities while interest 7. Other Disclosures _| dJuH¥$V {H$`m OmZm Mm{hE VWm B§Q>aoñQ>