Page 86 - Corporate Finance PDF Final new link

P. 86

NPP

86 Corporate Finance BRILLIANT’S

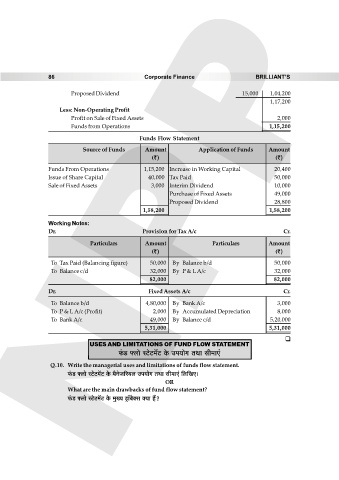

Proposed Dividend 15,000 1,04,200

1,17,200

Less: Non-Operating Profit

Profit on Sale of Fixed Assets 2,000

Funds from Operations 1,15,200

Funds Flow Statement

Source of Funds Amount Application of Funds Amount

(`) (`)

Funds From Operations 1,15,200 Increase in Working Capital 20,400

Issue of Share Capital 40,000 Tax Paid 50,000

Sale of Fixed Assets 3,000 Interim Dividend 10,000

Purchase of Fixed Assets 49,000

Proposed Dividend 28,800

1,58,200 1,58,200

Working Notes:

Dr. Provision for Tax A/c Cr.

Particulars Amount Particulars Amount

(`) (`)

To Tax Paid (Balancing figure) 50,000 By Balance b/d 50,000

To Balance c/d 32,000 By P & L A/c 32,000

82,000 82,000

Dr. Fixed Assets A/c Cr.

To Balance b/d 4,80,000 By Bank A/c 3,000

To P & L A/c (Profit) 2,000 By Accumulated Depreciation 8,000

To Bank A/c 49,000 By Balance c/d 5,20,000

5,31,000 5,31,000

USES AND LIMITATIONS OF FUND FLOW STATEMENT

’§$S> âbmo ñQ>oQ>‘|Q> Ho$ Cn¶moJ VWm gr‘mE§

Q.10. Write the managerial uses and limitations of funds flow statement.

’§$S> âbmo ñQ>oQ>‘|Q> Ho$ ‘¡ZoO[a¶b Cn¶moJ VWm gr‘mE§ {b{IE&

OR

What are the main drawbacks of fund flow statement?

’§$S> âbmo ñQ>oQ>‘|Q> Ho$ ‘w»¶ S´>m°~¡³g ³¶m h¢?