Page 205 - pwc-lease-accounting-guide_Neat

P. 205

Modification and remeasurement of a lease

At lease inception, Lessor Corp determines that the lease is an operating lease because none of the

criteria in ASC 842-10-25-2 are met. Lessor Corp calculates a straight-line rental revenue amount of

$162,490 annually.

At the beginning of year 4 of the lease, Lessee Corp and Lessor Corp agree to extend the lease term for

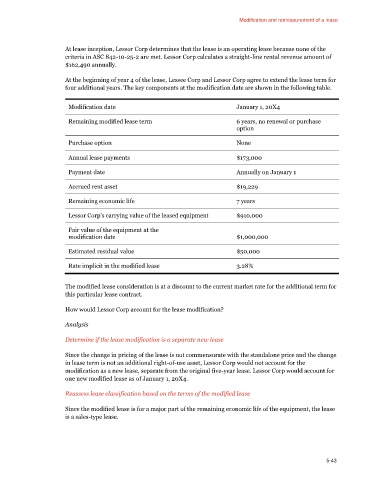

four additional years. The key components at the modification date are shown in the following table.

Modification date January 1, 20X4

Remaining modified lease term 6 years, no renewal or purchase

option

Purchase option None

Annual lease payments $173,000

Payment date Annually on January 1

Accrued rent asset $19,229

Remaining economic life 7 years

Lessor Corp’s carrying value of the leased equipment $910,000

Fair value of the equipment at the

modification date $1,000,000

Estimated residual value $50,000

Rate implicit in the modified lease 3.28%

The modified lease consideration is at a discount to the current market rate for the additional term for

this particular lease contract.

How would Lessor Corp account for the lease modification?

Analysis

Determine if the lease modification is a separate new lease

Since the change in pricing of the lease is not commensurate with the standalone price and the change

in lease term is not an additional right-of-use asset, Lessor Corp would not account for the

modification as a new lease, separate from the original five-year lease. Lessor Corp would account for

one new modified lease as of January 1, 20X4.

Reassess lease classification based on the terms of the modified lease

Since the modified lease is for a major part of the remaining economic life of the equipment, the lease

is a sales-type lease.

5-43