Page 206 - pwc-lease-accounting-guide_Neat

P. 206

Modification and remeasurement of a lease

Account for the modified lease

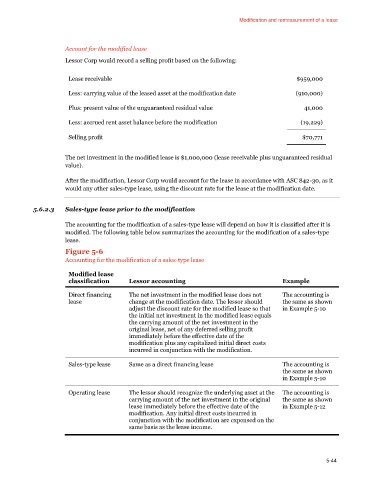

Lessor Corp would record a selling profit based on the following:

Lease receivable $959,000

Less: carrying value of the leased asset at the modification date (910,000)

Plus: present value of the unguaranteed residual value 41,000

Less: accrued rent asset balance before the modification (19,229)

Selling profit $70,771

The net investment in the modified lease is $1,000,000 (lease receivable plus unguaranteed residual

value).

After the modification, Lessor Corp would account for the lease in accordance with ASC 842-30, as it

would any other sales-type lease, using the discount rate for the lease at the modification date.

5.6.2.3 Sales-type lease prior to the modification

The accounting for the modification of a sales-type lease will depend on how it is classified after it is

modified. The following table below summarizes the accounting for the modification of a sales-type

lease.

Figure 5-6

Accounting for the modification of a sales-type lease

Modified lease

classification Lessor accounting Example

Direct financing The net investment in the modified lease does not The accounting is

lease change at the modification date. The lessor should the same as shown

adjust the discount rate for the modified lease so that in Example 5-10

the initial net investment in the modified lease equals

the carrying amount of the net investment in the

original lease, net of any deferred selling profit

immediately before the effective date of the

modification plus any capitalized initial direct costs

incurred in conjunction with the modification.

Sales-type lease Same as a direct financing lease The accounting is

the same as shown

in Example 5-10

Operating lease The lessor should recognize the underlying asset at the The accounting is

carrying amount of the net investment in the original the same as shown

lease immediately before the effective date of the in Example 5-12

modification. Any initial direct costs incurred in

conjunction with the modification are expensed on the

same basis as the lease income.

5-44