Page 39 - RB GRENADA ANNUAL REPORT 2025_ONLINE

P. 39

• 39

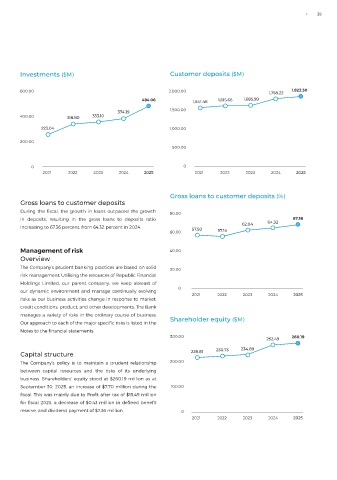

Investments ($M) Customer deposits ($M)

600.00 2,000.00 1,758.22 1,822.30

484.06 1,541.46 1,615.66 1,685.99

374.19 1,500.00

400.00 318.80 333.10

223.04 1,000.00

200.00

500.00

0 0

2021 2022 2023 2024 2025 2021 2022 2023 2024 2025

Gross loans to customer deposits (%)

Gross loans to customer deposits

During the fiscal, the growth in loans outpaced the growth 80.00

in deposits, resulting in the gross loans to deposits ratio 67.36

62.04 64.32

increasing to 67.36 percent, from 64.32 percent in 2024. 57.50

60.00 57.14

Management of risk 40.00

Overview

The Company’s prudent banking practices are based on solid 20.00

risk management. Utilising the resources of Republic Financial

Holdings Limited, our parent company, we keep abreast of

0

our dynamic environment and manage continually evolving 2021 2022 2023 2024 2025

risks as our business activities change in response to market,

credit conditions, product, and other developments. The Bank

manages a variety of risks in the ordinary course of business.

Our approach to each of the major specific risks is listed in the Shareholder equity ($M)

Notes to the financial statements.

300.00 252.49 260.19

Capital structure 228.81 230.73 234.89

The Company’s policy is to maintain a prudent relationship 200.00

between capital resources and the risks of its underlying

business. Shareholders’ equity stood at $260.19 million as at

September 30, 2025, an increase of $7.70 million during the 100.00

fiscal. This was mainly due to Profit after tax of $15.49 million

for fiscal 2025, a decrease of $0.43 million in defined benefit

reserve, and dividend payment of $7.36 million. 0

2021 2022 2023 2024 2025