Page 11 - tmp

P. 11

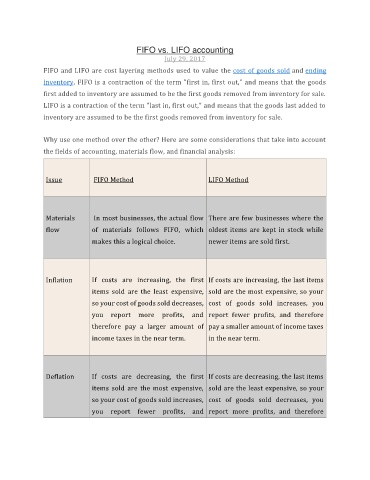

FIFO vs. LIFO accounting

July 29, 2017

FIFO and LIFO are cost layering methods used to value the cost of goods sold and ending

inventory. FIFO is a contraction of the term "first in, first out," and means that the goods

first added to inventory are assumed to be the first goods removed from inventory for sale.

LIFO is a contraction of the term "last in, first out," and means that the goods last added to

inventory are assumed to be the first goods removed from inventory for sale.

Why use one method over the other? Here are some considerations that take into account

the fields of accounting, materials flow, and financial analysis:

Issue FIFO Method LIFO Method

Materials In most businesses, the actual flow There are few businesses where the

flow of materials follows FIFO, which oldest items are kept in stock while

makes this a logical choice. newer items are sold first.

Inflation If costs are increasing, the first If costs are increasing, the last items

items sold are the least expensive, sold are the most expensive, so your

so your cost of goods sold decreases, cost of goods sold increases, you

you report more profits, and report fewer profits, and therefore

therefore pay a larger amount of pay a smaller amount of income taxes

income taxes in the near term. in the near term.

Deflation If costs are decreasing, the first If costs are decreasing, the last items

items sold are the most expensive, sold are the least expensive, so your

so your cost of goods sold increases, cost of goods sold decreases, you

you report fewer profits, and report more profits, and therefore