Page 1682 - draft

P. 1682

U.S. PUBLIC FINANCE

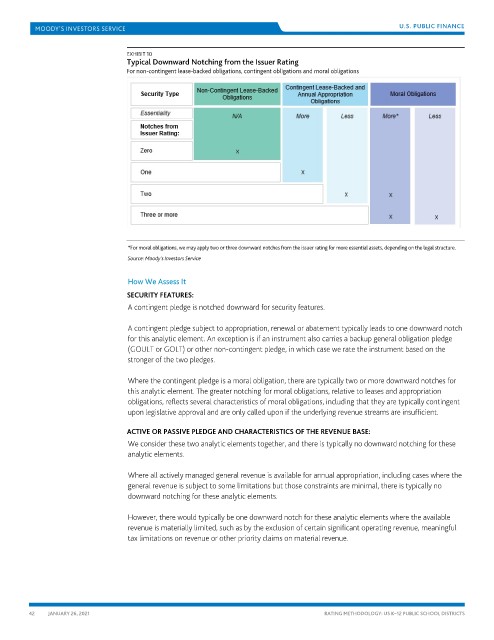

EXHIBIT 10

Typical Downward Notching from the Issuer Rating

For non-contingent lease-backed obligations, contingent obligations and moral obligations

*For moral obligations, we may apply two or three downward notches from the issuer rating for more essential assets, depending on the legal structure.

Source: Moody’s Investors Service

How We Assess It

SECURITY FEATURES:

A contingent pledge is notched downward for security features.

A contingent pledge subject to appropriation, renewal or abatement typically leads to one downward notch

for this analytic element. An exception is if an instrument also carries a backup general obligation pledge

(GOULT or GOLT) or other non-contingent pledge, in which case we rate the instrument based on the

stronger of the two pledges.

Where the contingent pledge is a moral obligation, there are typically two or more downward notches for

this analytic element. The greater notching for moral obligations, relative to leases and appropriation

obligations, reflects several characteristics of moral obligations, including that they are typically contingent

upon legislative approval and are only called upon if the underlying revenue streams are insufficient.

ACTIVE OR PASSIVE PLEDGE AND CHARACTERISTICS OF THE REVENUE BASE:

We consider these two analytic elements together, and there is typically no downward notching for these

analytic elements.

Where all actively managed general revenue is available for annual appropriation, including cases where the

general revenue is subject to some limitations but those constraints are minimal, there is typically no

downward notching for these analytic elements.

However, there would typically be one downward notch for these analytic elements where the available

revenue is materially limited, such as by the exclusion of certain significant operating revenue, meaningful

tax limitations on revenue or other priority claims on material revenue.

42 JANUARY 26, 2021 RATING METHODOLOGY: US K–12 PUBLIC SCHOOL DISTRICTS