Page 39 - cfi-Accounting-eBook

P. 39

The Corporate Finance Institute Accounting

Repairs and Replacements of PPE

The nature of PPE assets is that some of these assets need to be

regularly fixed or replaced to combat equipment failures or to adopt

more sophisticated technology. For example, it is normal for companies

to repair or replace old factories or automobiles with new assets when

necessary. The general rule in accounting for repairs and replacements

is that repairs and maintenance work is expensed while replacements

of assets are capitalized. Repairs are easy to record, it is simply a debit

to repair or maintenance expense and a credit to cash. Replacements,

however, are a bit more complicated. For replacements, the old cost of

the asset is derecognized from the company’s books and the new cost

of the replacement is recorded/recognized.

Bundled Purchases

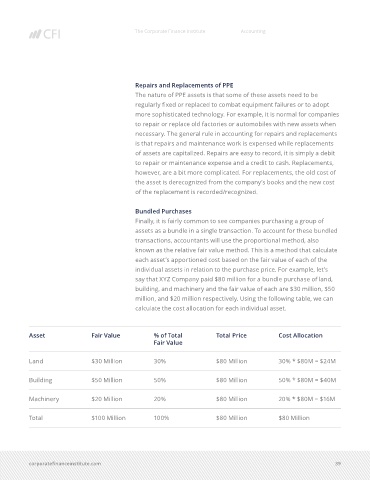

Finally, it is fairly common to see companies purchasing a group of

assets as a bundle in a single transaction. To account for these bundled

transactions, accountants will use the proportional method, also

known as the relative fair value method. This is a method that calculate

each asset’s apportioned cost based on the fair value of each of the

individual assets in relation to the purchase price. For example, let’s

say that XYZ Company paid $80 million for a bundle purchase of land,

building, and machinery and the fair value of each are $30 million, $50

million, and $20 million respectively. Using the following table, we can

calculate the cost allocation for each individual asset.

Asset Fair Value % of Total Total Price Cost Allocation

Fair Value

Land $30 Million 30% $80 Million 30% * $80M = $24M

Building $50 Million 50% $80 Million 50% * $80M = $40M

Machinery $20 Million 20% $80 Million 20% * $80M = $16M

Total $100 Million 100% $80 Million $80 Million

corporatefinanceinstitute.com 39