Page 140 - VIRANSH COACHING CLASSES

P. 140

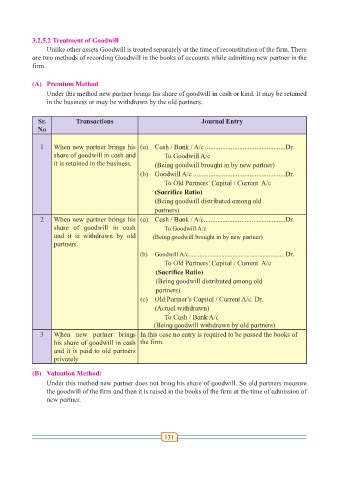

3.2.5.2 Treatment of Goodwill

Unlike other assets Goodwill is treated separately at the time of reconstitution of the firm. There

are two methods of recording Goodwill in the books of accounts while admitting new partner in the

firm.

(A) Premium Method

Under this method new partner brings his share of goodwill in cash or kind. It may be retained

in the business or may be withdrawn by the old partners.

Sr. Transactions Journal Entry

No

1 When new partner brings his (a) Cash / Bank / A/c ...............................................Dr.

share of goodwill in cash and To Goodwill A/c

it is retained in the business. (Being goodwill brought in by new partner)

(b) Goodwill A/c ......................................................Dr.

To Old Partners’ Capital / Current A/c

(Sacrifice Ratio)

(Being goodwill distributed among old

partners)

2 When new partner brings his (a) Cash / Bank / A/c.............................. .................Dr.

share of goodwill in cash To Goodwill A/c

and it is withdrawn by old (Being goodwill brought in by new partner)

partners.

(b) Goodwill A/c........................................... .................. Dr.

To Old Partners’ Capital / Current A/c

(Sacrifice Ratio)

(Being goodwill distributed among old

partners)

(c) Old Partner’s Capital / Current A/c. Dr.

(Actual withdrawn)

To Cash / Bank A/c

(Being goodwill withdrawn by old partners)

3 When new partner brings In this case no entry is required to be passed the books of

his share of goodwill in cash the firm.

and it is paid to old partners

privately

(B) Valuation Method:

Under this method new partner does not bring his share of goodwill. So old partners measure

the goodwill of the firm and then it is raised in the books of the firm at the time of admission of

new partner.

131