Page 362 - VIRANSH COACHING CLASSES

P. 362

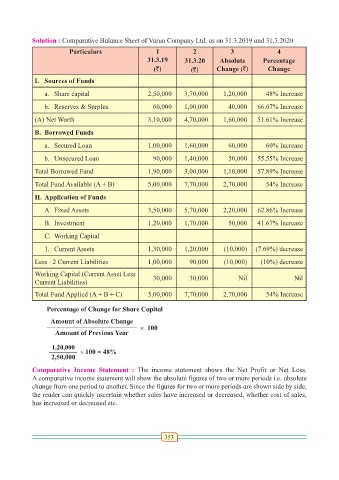

Solution : Comparative Balance Sheet of Varun Company Ltd. as on 31.3.2019 and 31.3.2020

Particulars 1 2 3 4

31.3.19 31.3.20 Absolute Percentage

(`) (`) Change (`) Change

I. Sources of Funds

a. Share capital 2,50,000 3,70,000 1,20,000 48% Increase

b. Reserves & Surplus 60,000 1,00,000 40,000 66.67% Increase

(A) Net Worth 3,10,000 4,70,000 1,60,000 51.61% Increase

B. Borrowed Funds

a. Secured Loan 1,00,000 1,60,000 60,000 60% Increase

b. Unsecured Loan 90,000 1,40,000 50,000 55.55% Increase

Total Borrowed Fund 1,90,000 3,00,000 1,10,000 57.89% Increase

Total Fund Available (A + B) 5,00,000 7,70,000 2,70,000 54% Increase

II. Application of Funds

A. Fixed Assets 3,50,000 5,70,000 2,20,000 62.86% Increase

B. Investment 1,20,000 1,70,000 50,000 41.67% Increase

C. Working Capital

1. Current Assets 1,30,000 1,20,000 (10,000) (7.69%) decrease

Less : 2 Current Liabilities 1,00,000 90,000 (10,000) (10%) decrease

Working Capital (Current Asset Less 30,000 30,000 Nil Nil

Current Liabilities)

Total Fund Applied (A + B + C) 5,00,000 7,70,000 2,70,000 54% Increase

Percentage of Change for Share Capital

Amount of Absolute Change

× 100

Amount of Previous Year

1,20,000 × 100 = 48%

2,50,000

Comparative Income Statement : The income statement shows the Net Profit or Net Loss.

A comparative income statement will show the absolute figures of two or more periods i.e. absolute

change from one period to another. Since the figures for two or more periods are shown side by side,

the reader can quickly ascertain whether sales have increased or decreased, whether cost of sales,

has increased or decreased etc.

353