Page 231 - ACFE Fraud Reports 2009_2020

P. 231

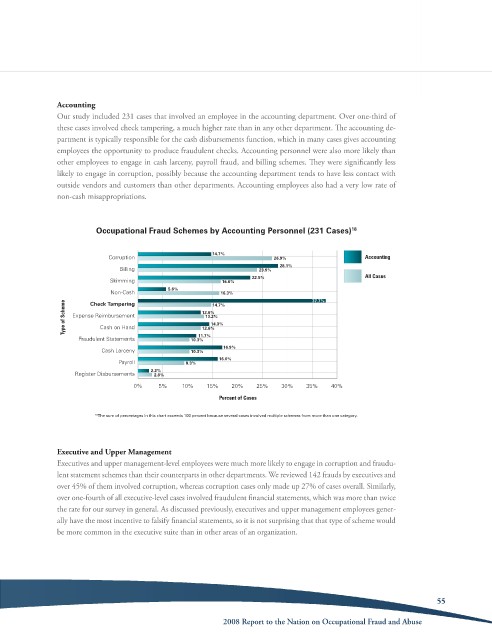

Accounting

our study included 231 cases that involved an employee in the accounting department. over one-third of

these cases involved check tampering, a much higher rate than in any other department. The accounting de-

partment is typically responsible for the cash disbursements function, which in many cases gives accounting

employees the opportunity to produce fraudulent checks. accounting personnel were also more likely than

other employees to engage in cash larceny, payroll fraud, and billing schemes. They were significantly less

likely to engage in corruption, possibly because the accounting department tends to have less contact with

outside vendors and customers than other departments. accounting employees also had a very low rate of

non-cash misappropriations.

Occupational Fraud Schemes by Accounting Personnel (231 Cases) 18

14.7%

Corruption 26.9% Accounting

28.1%

Billing 23.9%

22.5% All Cases

Skimming 16.6%

5.6%

Non-Cash 14.7% 37.7%

16.3%

Type of Scheme Expense Reimbursement 12.6% 14.3%

Check Tampering

13.2%

Cash on Hand

12.6%

11.7%

Fraudulent Statements 10.3%

16.9%

Cash Larceny 10.3%

16.0%

Payroll 9.3%

2.2%

Register Disbursements 2.8%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Percent of Cases

18 The sum of percentages in this chart exceeds 100 percent because several cases involved multiple schemes from more than one category.

Executive and Upper Management

executives and upper management-level employees were much more likely to engage in corruption and fraudu-

lent statement schemes than their counterparts in other departments. We reviewed 142 frauds by executives and

over 45% of them involved corruption, whereas corruption cases only made up 27% of cases overall. similarly,

over one-fourth of all executive-level cases involved fraudulent financial statements, which was more than twice

the rate for our survey in general. as discussed previously, executives and upper management employees gener-

ally have the most incentive to falsify financial statements, so it is not surprising that that type of scheme would

be more common in the executive suite than in other areas of an organization.

55

2008 Report to the Nation on occupational Fraud and abuse