Page 235 - ACFE Fraud Reports 2009_2020

P. 235

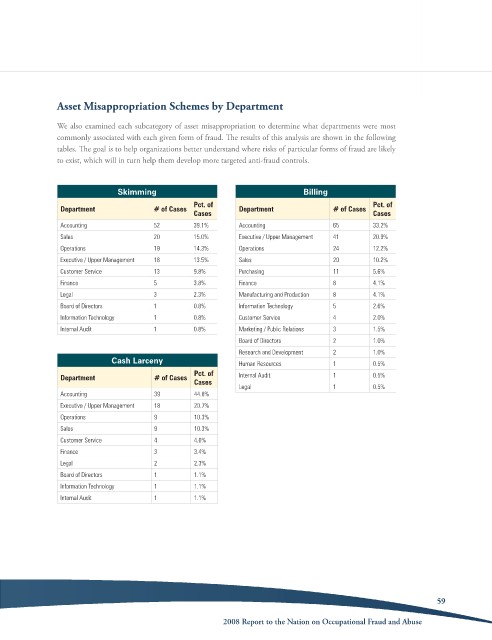

Asset Misappropriation Schemes by Department

We also examined each subcategory of asset misappropriation to determine what departments were most

commonly associated with each given form of fraud. The results of this analysis are shown in the following

tables. The goal is to help organizations better understand where risks of particular forms of fraud are likely

to exist, which will in turn help them develop more targeted anti-fraud controls.

Skimming Billing

Pct. of Pct. of

Department # of Cases Department # of Cases

Cases Cases

Accounting 52 39.1% Accounting 65 33.2%

Sales 20 15.0% Executive / Upper Management 41 20.9%

Operations 19 14.3% Operations 24 12.2%

Executive / Upper Management 18 13.5% Sales 20 10.2%

Customer Service 13 9.8% Purchasing 11 5.6%

Finance 5 3.8% Finance 8 4.1%

Legal 3 2.3% Manufacturing and Production 8 4.1%

Board of Directors 1 0.8% Information Technology 5 2.6%

Information Technology 1 0.8% Customer Service 4 2.0%

Internal Audit 1 0.8% Marketing / Public Relations 3 1.5%

Board of Directors 2 1.0%

Research and Development 2 1.0%

Cash Larceny Human Resources 1 0.5%

Pct. of

Department # of Cases Internal Audit 1 0.5%

Cases

Legal 1 0.5%

Accounting 39 44.8%

Executive / Upper Management 18 20.7%

Operations 9 10.3%

Sales 9 10.3%

Customer Service 4 4.6%

Finance 3 3.4%

Legal 2 2.3%

Board of Directors 1 1.1%

Information Technology 1 1.1%

Internal Audit 1 1.1%

59

2008 Report to the Nation on occupational Fraud and abuse