Page 31 - Banking Fiannce March 2018

P. 31

ARTICLE

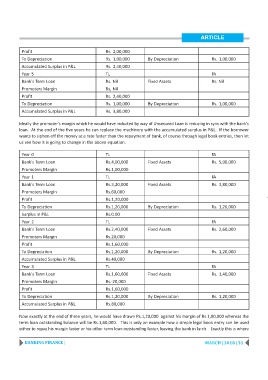

Profit Rs. 2,00,000

To Depreciation Rs. 1,00,000 By Depreciation Rs. 1,00,000

Accumulated Surplus in P&L Rs. 2,40,000

Year 5 TL FA

Bank's Term Loan Rs. Nil Fixed Assets Rs. Nil

Promoters Margin Rs, Nil

Profit Rs. 2,40,000

To Depreciation Rs. 1,00,000 By Depreciation Rs. 1,00,000

Accumulated Surplus in P&L Rs. 3,80,000

Ideally the promoter's margin which he would have inducted by way of Unsecured Loan is reducing in sync with the bank's

loan. At the end of the five years he can replace the machinery with the accumulated surplus in P&L. If the borrower

wants to siphon off the money at a rate faster than the repayment of bank, of course through legal book entries, then let

us see how it is going to change in the above equation.

Year 0 TL FA

Bank's Term Loan Rs.4,00,000 Fixed Assets Rs. 5,00,000

Promoters Margin Rs.1,00,000

Year 1 TL FA

Bank's Term Loan Rs.3,20,000 Fixed Assets Rs. 3,80,000

Promoters Margin Rs.60,000

Profit Rs.1,20,000

To Depreciation Rs.1,20,000 By Depreciation Rs. 1,20,000

Surplus in P&L Rs.0.00

Year 2 TL FA

Bank's Term Loan Rs.2,40,000 Fixed Assets Rs. 2,60,000

Promoters Margin Rs.20,000

Profit Rs.1,60,000

To Depreciation Rs.1,20,000 By Depreciation Rs. 1,20,000

Accumulated Surplus in P&L Rs.40,000

Year 3 TL FA

Bank's Term Loan Rs.1,60,000 Fixed Assets Rs. 1,40,000

Promoters Margin Rs.-20,000

Profit Rs.1,60,000

To Depreciation Rs.1,20,000 By Depreciation Rs. 1,20,000

Accumulated Surplus in P&L Rs.80,000

Now exactly at the end of three years, he would have drawn Rs.1,20,000 against his margin of Rs.1,00,000 whereas the

term loan outstanding balance will be Rs.1,60,000. This is only an example how a simple legal book entry can be used

either to repay his margin faster or his other term loan outstanding faster, leaving the bank in lurch. Exactly this is where

BANKING FINANCE | MARCH | 2018 | 31