Page 10 - FSUOGM Week 21 2021

P. 10

FSUOGM COMMENTARY FSUOGM

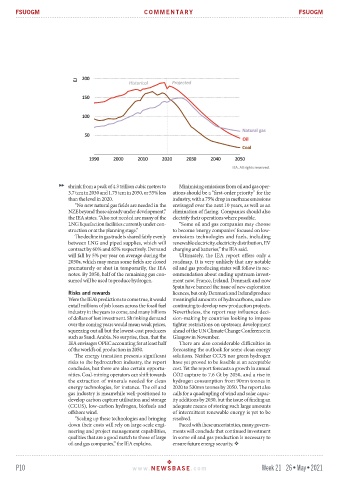

shrink from a peak of 4.3 trillion cubic metres to Minimising emissions from oil and gas oper-

3.7 tcm in 2030 and 1.75 tcm in 2050, or 55% less ations should be a “first-order priority” for the

than the level in 2020. industry, with a 75% drop in methane emissions

“No new natural gas fields are needed in the envisaged over the next 10 years, as well as an

NZE beyond those already under development,” elimination of flaring. Companies should also

the IEA states. “Also not needed are many of the electrify their operations where possible.

LNG liquefaction facilities currently under con- “Some oil and gas companies may choose

struction or at the planning stage.” to become ‘energy companies’ focused on low‐

The decline in gas trade is shared fairly evenly emissions technologies and fuels, including

between LNG and piped supplies, which will renewable electricity, electricity distribution, EV

contract by 60% and 65% respectively. Demand charging and batteries,” the IEA said.

will fall by 5% per year on average during the Ultimately, the IEA report offers only a

2030s, which may mean some fields are closed roadmap. It is very unlikely that any notable

prematurely or shut in temporarily, the IEA oil and gas producing states will follow its rec-

notes. By 2050, half of the remaining gas con- ommendation about ending upstream invest-

sumed will be used to produce hydrogen. ment now. France, Ireland, Denmark and now

Spain have banned the issue of new exploration

Risks and rewards licences, but only Denmark and Ireland produce

Were the IEA’s predictions to come true, it would meaningful amounts of hydrocarbons, and are

entail millions of job losses across the fossil fuel continuing to develop new production projects.

industry in the years to come, and many billions Nevertheless, the report may influence deci-

of dollars of lost investment. Shrinking demand sion-making by countries looking to impose

over the coming years would mean weak prices, tighter restrictions on upstream development

squeezing out all but the lowest-cost producers ahead of the UN Climate Change Conference in

such as Saudi Arabia. No surprise, then, that the Glasgow in November.

IEA envisages OPEC accounting for at least half There are also considerable difficulties in

of the world’s oil production in 2050. forecasting the outlook for some clean energy

The energy transition presents significant solutions. Neither CCUS nor green hydrogen

risks to the hydrocarbon industry, the report have yet proved to be feasible at an acceptable

concludes, but there are also certain opportu- cost. Yet the report forecasts a growth in annual

nities. Coal-mining operators can shift towards CO2 capture to 7.6 Gt by 2050, and a rise in

the extraction of minerals needed for clean hydrogen consumption from 90mn tonnes in

energy technologies, for instance. The oil and 2020 to 530mn tonnes by 2050. The report also

gas industry is meanwhile well-positioned to calls for a quadrupling of wind and solar capac-

develop carbon capture utilisation and storage ity additions by 2030, but the issue of finding an

(CCUS), low-carbon hydrogen, biofuels and adequate means of storing such large amounts

offshore wind. of intermittent renewable energy is yet to be

“Scaling up these technologies and bringing resolved.

down their costs will rely on large-scale engi- Faced with these uncertainties, many govern-

neering and project management capabilities, ments will conclude that continued investment

qualities that are a good match to those of large in some oil and gas production is necessary to

oil and gas companies,” the IEA explains. ensure future energy security.

P10 www. NEWSBASE .com Week 21 26•May•2021