Page 5 - NorthAmOil Week 14 2021

P. 5

NorthAmOil COMMENTARY NorthAmOil

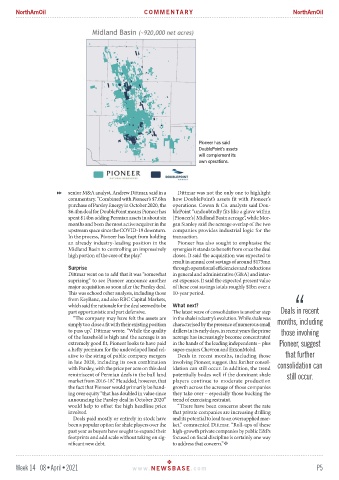

Pioneer has said

DoublePoint’s assets

will complement its

own operations.

senior M&A analyst, Andrew Dittmar, said in a Dittmar was not the only one to highlight

commentary. “Combined with Pioneer’s $7.6bn how DoublePoint’s assets fit with Pioneer’s

purchase of Parsley Energy in October 2020, the operations. Cowen & Co. analysts said Dou-

$6.4bn deal for DoublePoint means Pioneer has blePoint “undoubtedly fits like a glove within

spent $14bn adding Permian assets in about six [Pioneer’s] Midland Basin acreage”, while Mor-

months and been the most active acquirer in the gan Stanley said the acreage overlap of the two

upstream space since the COVID-19 downturn. companies provides industrial logic for the

In the process, Pioneer has leapt from holding transaction.

an already industry-leading position in the Pioneer has also sought to emphasise the

Midland Basin to controlling an impressively synergies it stands to benefit from once the deal

high portion of the core of the play.” closes. It said the acquisition was expected to

result in annual cost savings of around $175mn

Surprise through operational efficiencies and reductions

Dittmar went on to add that it was “somewhat in general and administrative (G&A) and inter-

suprising” to see Pioneer announce another est expenses. It said the expected present value

major acquisition so soon after the Parsley deal. of these cost savings totals roughly $1bn over a

This was echoed other analysts, including those 10-year period.

from KeyBanc, and also RBC Capital Markets,

which said the rationale for the deal seemed to be What next?

part opportunistic and part defensive. The latest wave of consolidation is another step Deals in recent

“The company may have felt the assets are in the shale industry’s evolution. While shale was

simply too close a fit with their existing position characterised by the presence of numerous small months, including

to pass up,” Dittmar wrote. “While the quality drillers in its early days, in recent years the prime those involving

of the leasehold is high and the acreage is an acreage has increasingly become concentrated

extremely good fit, Pioneer looks to have paid in the hands of the leading independents – plus Pioneer, suggest

a hefty premium for the undeveloped land rel- super-majors Chevron and ExxonMobil.

ative to the string of public company mergers Deals in recent months, including those that further

in late 2020, including its own combination involving Pioneer, suggest that further consol-

with Parsley, with the price per acre on this deal idation can still occur. In addition, the trend consolidation can

reminiscent of Permian deals in the bull land potentially bodes well if the dominant shale still occur.

market from 2016-18.” He added, however, that players continue to moderate production

the fact that Pioneer would primarily be hand- growth across the acreage of those companies

ing over equity “that has doubled in value since they take over – especially those bucking the

announcing the Parsley deal in October 2020” trend of exercising restraint.

would help to offset the high headline price “There have been concerns about the rate

involved. that private companies are increasing drilling

Deals paid mostly or entirely in stock have and its potential to lead to an oversupplied mar-

been a popular option for shale players over the ket,” commented Dittmar. “Roll-ups of these

past year as buyers have sought to expand their high-growth private companies by public E&Ps

footprints and add scale without taking on sig- focused on fiscal discipline is certainly one way

nificant new debt. to address that concern.”

Week 14 08•April•2021 www. NEWSBASE .com P5