Page 166 - รวมเล่มเอกคำสอน Credit managment 2564-printed 2565 with watermark

P. 166

เอกสารคําสอนวิชาการจัดการสินเช่อ ผศ.ดร.ฐิติมา ไชยะกุล. 2564

ื

(Credit Mangement) 03759342 คณะวิทยาการจัดการ มหาวิทยาลัยเกษตรศาสตร์

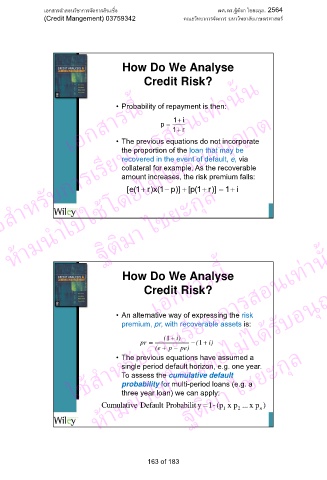

How Do We Analyse

ใช้สําหรับการเรียนการสอนเท่านั้น

Credit Risk?

เอกสารนี้ p 1 r i

1 ( x ) rมได้รับอนุญาต

• Probability of repayment is then:

1

• The previous equations do not incorporate

the proportion of the loan that may be

recovered in the event of default, e, via

่

collateral for example. As the recoverable

โดยไ

amount increases, the risk premium falls:

p

1 ( e [

)]

)]

1

i

r

1 ( p [

ห้ามนําไปใช้ ฐิติมา ไชยะกุล

ใช้สําหรับการเรียนการสอนเท่านั้น

เอกสารนี้

โดยไมได้รับอนุญาต

How Do We Analyse

Credit Risk?

• An alternative way of expressing the risk

premium, pr, with recoverable assets is:

( 1 i) ่

(

pr 1 i)

(e p pe)

• The previous equations have assumed a

ห้ามนําไปใช้ ฐิติม - 1 (pา ไชยะกุล

single period default horizon, e.g. one year.

To assess the cumulative default

probability for multi-period loans (e.g. a

three year loan) we can apply:

y

...

p

x

)

p

x

Default

Cumulative

Probabilit

n

2

1

163 of 183