Page 168 - รวมเล่มเอกคำสอน Credit managment 2564-printed 2565 with watermark

P. 168

เอกสารคําสอนวิชาการจัดการสินเช่อ ผศ.ดร.ฐิติมา ไชยะกุล. 2564

ื

(Credit Mangement) 03759342 คณะวิทยาการจัดการ มหาวิทยาลัยเกษตรศาสตร์

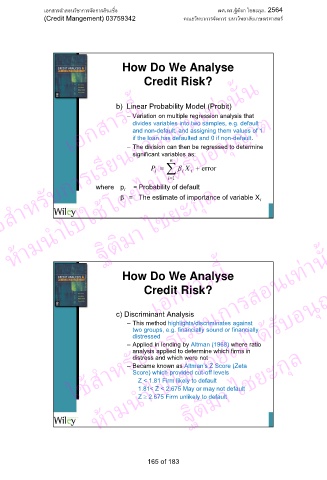

How Do We Analyse

b) Linear Probability Model (Probit)นั้น

เอกสารนี้ Credit Risk?

ใช้สําหรับการเรียนการสอนเท่า

1ด้รับอนุญาต

– Variation on multiple regression analysis that

divides variables into two samples, e.g. default

and non-default, and assigning them values of 1

if the loan has defaulted and 0 if non-default.

– The division can then be regressed to determine

โดยไมไ

n

่

P

X

β

i

i

i

i

= Probability of default

where p i significant variables as: error i

ห้ามนําไปใช้ ฐิติมา ไชยะกุล

= The estimate of importance of variable X

ใช้สําหรับการเรียนการสอนเท่านั้น

เอกสารนี้

โดยไมได้รับอนุญาต

How Do We Analyse

Credit Risk?

c) Discriminant Analysis

– This method highlights/discriminates against

two groups, e.g. financially sound or financially

distressed ่

1.81< Z < 2.675 May or may not defaultชยะกุล

– Applied in lending by Altman (1968) where ratio

analysis applied to determine which firms in

ห้ามนําไปใช้ ฐิติมา ไ

distress and which were not

– Became known as Altman’s Z Score (Zeta

Score) which provided cut-off levels

Z < 1.81 Firm likely to default

Z 2.675 Firm unlikely to default

165 of 183