Page 155 - Internal Auditing Standards

P. 155

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

12.4 Reporting

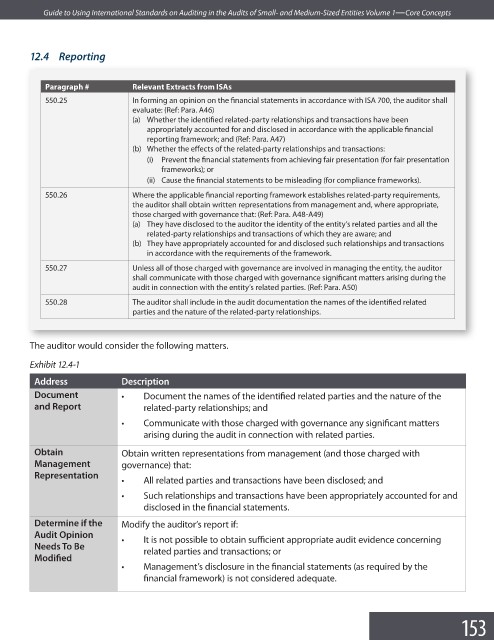

Paragraph # Relevant Extracts from ISAs

550.25 In forming an opinion on the financial statements in accordance with ISA 700, the auditor shall

evaluate: (Ref: Para. A46)

(a) Whether the identified related-party relationships and transactions have been

appropriately accounted for and disclosed in accordance with the applicable fi nancial

reporting framework; and (Ref: Para. A47)

(b) Whether the effects of the related-party relationships and transactions:

(i) Prevent the financial statements from achieving fair presentation (for fair presentation

frameworks); or

(ii) Cause the financial statements to be misleading (for compliance frameworks).

550.26 Where the applicable financial reporting framework establishes related-party requirements,

the auditor shall obtain written representations from management and, where appropriate,

those charged with governance that: (Ref: Para. A48-A49)

(a) They have disclosed to the auditor the identity of the entity’s related parties and all the

related-party relationships and transactions of which they are aware; and

(b) They have appropriately accounted for and disclosed such relationships and transactions

in accordance with the requirements of the framework.

550.27 Unless all of those charged with governance are involved in managing the entity, the auditor

shall communicate with those charged with governance significant matters arising during the

audit in connection with the entity’s related parties. (Ref: Para. A50)

550.28 The auditor shall include in the audit documentation the names of the identifi ed related

parties and the nature of the related-party relationships.

The auditor would consider the following matters.

Exhibit 12.4-1

Address Description

Document • Document the names of the identified related parties and the nature of the

and Report related-party relationships; and

• Communicate with those charged with governance any signifi cant matters

arising during the audit in connection with related parties.

Obtain Obtain written representations from management (and those charged with

Management governance) that:

Representation

• All related parties and transactions have been disclosed; and

• Such relationships and transactions have been appropriately accounted for and

disclosed in the fi nancial statements.

Determine if the Modify the auditor’s report if:

Audit Opinion • It is not possible to obtain sufficient appropriate audit evidence concerning

Needs To Be

related parties and transactions; or

Modifi ed

• Management’s disclosure in the financial statements (as required by the

financial framework) is not considered adequate.

153