Page 182 - Internal Auditing Standards

P. 182

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

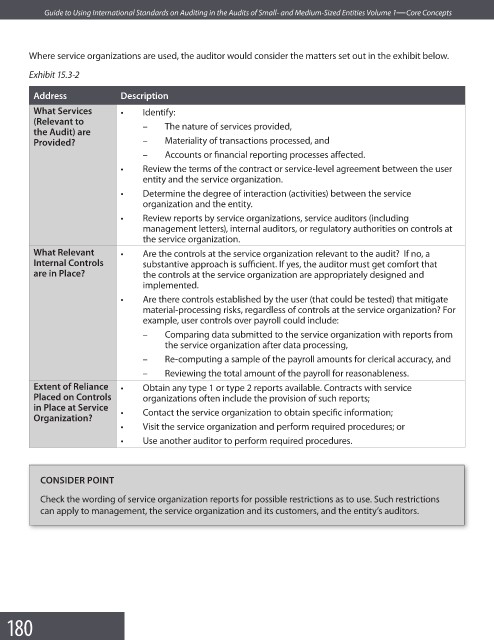

Where service organizations are used, the auditor would consider the matters set out in the exhibit below.

Exhibit 15.3-2

Address Description

What Services • Identify:

(Relevant to – The nature of services provided,

the Audit) are

Provided? – Materiality of transactions processed, and

– Accounts or financial reporting processes aff ected.

• Review the terms of the contract or service-level agreement between the user

entity and the service organization.

• Determine the degree of interaction (activities) between the service

organization and the entity.

• Review reports by service organizations, service auditors (including

management letters), internal auditors, or regulatory authorities on controls at

the service organization.

What Relevant • Are the controls at the service organization relevant to the audit? If no, a

Internal Controls substantive approach is sufficient. If yes, the auditor must get comfort that

are in Place? the controls at the service organization are appropriately designed and

implemented.

• Are there controls established by the user (that could be tested) that mitigate

material-processing risks, regardless of controls at the service organization? For

example, user controls over payroll could include:

– Comparing data submitted to the service organization with reports from

the service organization after data processing,

– Re-computing a sample of the payroll amounts for clerical accuracy, and

– Reviewing the total amount of the payroll for reasonableness.

Extent of Reliance • Obtain any type 1 or type 2 reports available. Contracts with service

Placed on Controls organizations often include the provision of such reports;

in Place at Service • Contact the service organization to obtain specifi c information;

Organization?

• Visit the service organization and perform required procedures; or

• Use another auditor to perform required procedures.

CONSIDER POINT

Check the wording of service organization reports for possible restrictions as to use. Such restrictions

can apply to management, the service organization and its customers, and the entity’s auditors.

180