Page 64 - Internal Auditing Standards

P. 64

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

This requires pertinent information to be identified, captured, and communicated/distributed on a timely

basis to personnel (at all levels of the entity) who need it for decision-making.

An information system consists of infrastructure (physical and hardware components), software, people,

procedures, and data. Many information systems make extensive use of information technology (IT). They

identify, capture, process, and distribute information supporting the achievement of financial reporting and

internal control objectives.

An information system relevant to financial reporting objectives includes the entity’s business processes and

accounting system, as set out below.

Exhibit 5.5-1

Business Processes Business processes are structured sets of activities designed to produce a specifi ed

(Sales, Purchases, output. They result in transactions being recorded, processed, and reported by the

Payroll, etc.) information system.

Accounting This includes accounting software, electronic spreadsheets, and the policies and

System procedures used to prepare periodic financial reports and the period-end fi nancial

statements and disclosures.

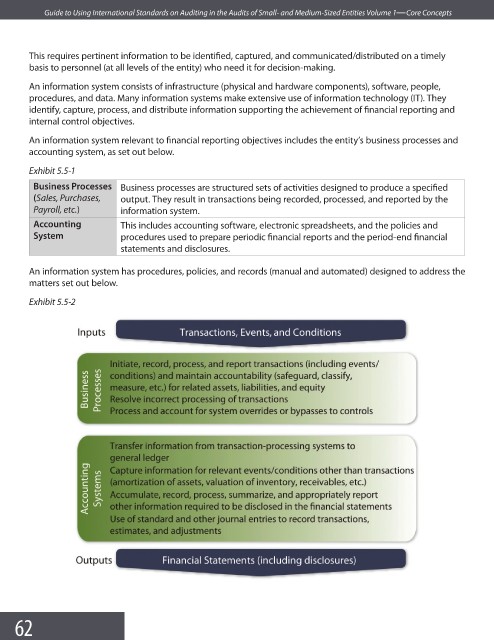

An information system has procedures, policies, and records (manual and automated) designed to address the

matters set out below.

Exhibit 5.5-2

62