Page 68 - Internal Auditing Standards

P. 68

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

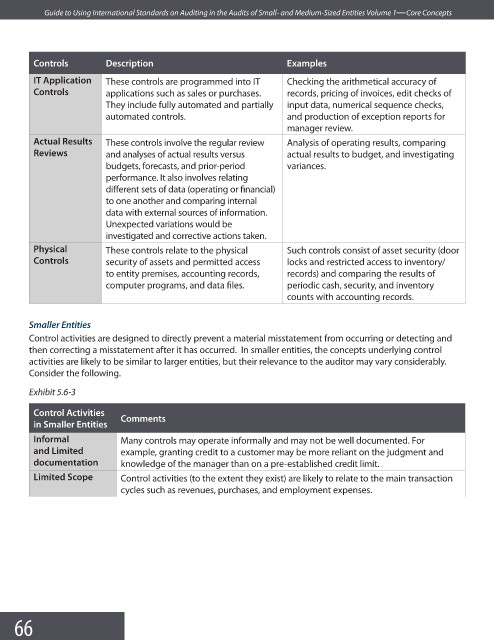

Controls Description Examples

IT Application These controls are programmed into IT Checking the arithmetical accuracy of

Controls applications such as sales or purchases. records, pricing of invoices, edit checks of

They include fully automated and partially input data, numerical sequence checks,

automated controls. and production of exception reports for

manager review.

Actual Results These controls involve the regular review Analysis of operating results, comparing

Reviews and analyses of actual results versus actual results to budget, and investigating

budgets, forecasts, and prior-period variances.

performance. It also involves relating

different sets of data (operating or fi nancial)

to one another and comparing internal

data with external sources of information.

Unexpected variations would be

investigated and corrective actions taken.

Physical These controls relate to the physical Such controls consist of asset security (door

Controls security of assets and permitted access locks and restricted access to inventory/

to entity premises, accounting records, records) and comparing the results of

computer programs, and data fi les. periodic cash, security, and inventory

counts with accounting records.

Smaller Entities

Control activities are designed to directly prevent a material misstatement from occurring or detecting and

then correcting a misstatement after it has occurred. In smaller entities, the concepts underlying control

activities are likely to be similar to larger entities, but their relevance to the auditor may vary considerably.

Consider the following.

Exhibit 5.6-3

Control Activities

Comments

in Smaller Entities

Informal Many controls may operate informally and may not be well documented. For

and Limited example, granting credit to a customer may be more reliant on the judgment and

documentation knowledge of the manager than on a pre-established credit limit.

Limited Scope Control activities (to the extent they exist) are likely to relate to the main transaction

cycles such as revenues, purchases, and employment expenses.

66