Page 305 - International Taxation IRS Training Guides

P. 305

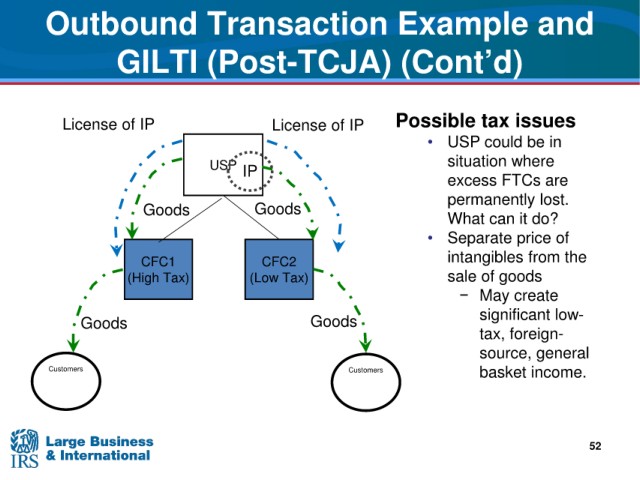

Outbound Transaction Example and

GILTI (Post-TCJA) (Cont’d)

Possible tax issues

License of IP License of IP

• USP

could be in

USP IP situation where

excess FTCs are

permanently

lost.

Goods Goods

What can it do?

• Separate price of

from the

CFC1 CFC2 intangibles

(High Tax) (Low Tax) sale of goods

create

− May

Goods Goods significant low-

tax, foreign-

source, general

Customers Customers basket income.

52