Page 306 - International Taxation IRS Training Guides

P. 306

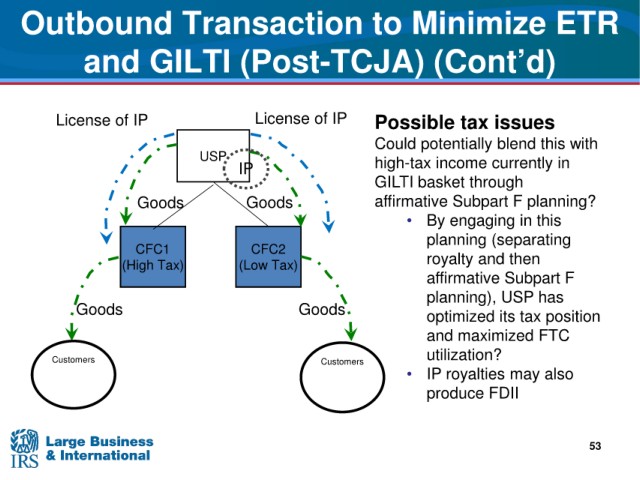

Outbound Transaction to Minimize ETR

and GILTI (Post-TCJA)

(Cont’d)

License of IP License of IP

Possible tax issues

Could potentially

blend this with

USP high-tax

income currently in

IP

through

GILTI basket

Goods Goods affirmative Subpart F planning?

engaging in this

• By

planning (separating

CFC1 CFC2

and then

(High Tax) (Low Tax) royalty

affirmative Subpart F

planning),

USP has

Goods Goods optimized its

tax position

and maximized FTC

utilization?

Customers Customers

• IP royalties

may also

produce FDII

53