Page 77 - IC26 LIFE INSURANCE FINANCE

P. 77

Where Specific Identification method is not applicable, The cost of inventories is valued by the following

methods;

FIFO ( First In First Out) Method

Weighted Average Cost

Cost of inventories in certain conditions:

The following methods may be used for convenience if the results approximate actual cost.

Standard Cost: It takes into account normal level of consumption of material and supplies, labour, efficiency

and capacity utilization. It must be regularly reviewed taking into consideration the current condition.

Retail Method: Normally applicable for retail trade. Cost of inventory is determined by reducing the gross

margin from the sale value of inventory.

Net Realisable Value: NRV means the estimated selling price in ordinary course of business, at the time of

valuation, less estimated cost of completion and estimated cost necessary to make the sale.

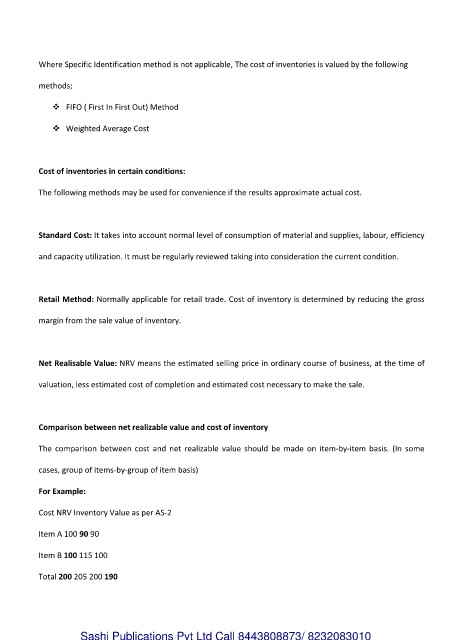

Comparison between net realizable value and cost of inventory

The comparison between cost and net realizable value should be made on item-by-item basis. (In some

cases, group of items-by-group of item basis)

For Example:

Cost NRV Inventory Value as per AS-2

Item A 100 90 90

Item B 100 115 100

Total 200 205 200 190

Sashi Publications Pvt Ltd Call 8443808873/ 8232083010