Page 69 - Risk Management in current scenario

P. 69

We may observe the volatility in the yield of 10-Year G-Sec from close to

11% by the end of year 2000, to November 2017 when the same yield

has fallen to close to 6.5%. Between these periods, the lowest yield that

the 10-Year G-Sec touched was in the year 2004, close to 5.5%.

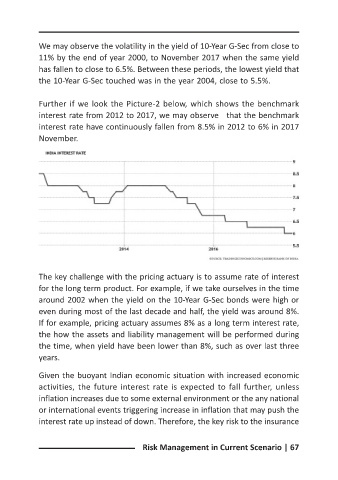

Further if we look the Picture-2 below, which shows the benchmark

interest rate from 2012 to 2017, we may observe that the benchmark

interest rate have continuously fallen from 8.5% in 2012 to 6% in 2017

November.

The key challenge with the pricing actuary is to assume rate of interest

for the long term product. For example, if we take ourselves in the time

around 2002 when the yield on the 10-Year G-Sec bonds were high or

even during most of the last decade and half, the yield was around 8%.

If for example, pricing actuary assumes 8% as a long term interest rate,

the how the assets and liability management will be performed during

the time, when yield have been lower than 8%, such as over last three

years.

Given the buoyant Indian economic situation with increased economic

activities, the future interest rate is expected to fall further, unless

inflation increases due to some external environment or the any national

or international events triggering increase in inflation that may push the

interest rate up instead of down. Therefore, the key risk to the insurance

Risk Management in Current Scenario | 67