Page 42 - P6 Slide Taxation - Lecture Day 2 - Trust

P. 42

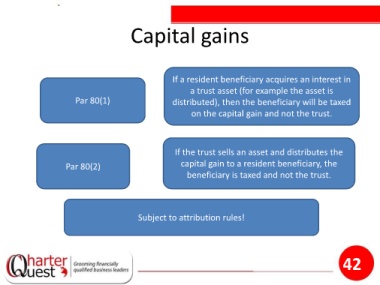

Capital gains

If a resident beneficiary acquires an interest in

a trust asset (for example the asset is

Par 80(1) distributed), then the beneficiary will be taxed

on the capital gain and not the trust.

If the trust sells an asset and distributes the

Par 80(2) capital gain to a resident beneficiary, the

beneficiary is taxed and not the trust.

Subject to attribution rules!

42