Page 21 - P6 Slide Taxation - Lecture Day 3 - VAT Part 3

P. 21

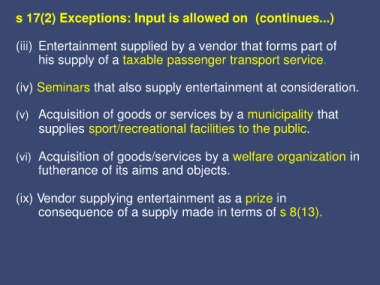

s 17(2) Exceptions: Input is allowed on (continues...)

(iii) Entertainment supplied by a vendor that forms part of

his supply of a taxable passenger transport service.

(iv) Seminars that also supply entertainment at consideration.

(v) Acquisition of goods or services by a municipality that

supplies sport/recreational facilities to the public.

(vi) Acquisition of goods/services by a welfare organization in

futherance of its aims and objects.

(ix) Vendor supplying entertainment as a prize in

consequence of a supply made in terms of s 8(13).