Page 121 - BA2 Integrated Workbook - Student 2017

P. 121

Standard costing and variance analysis

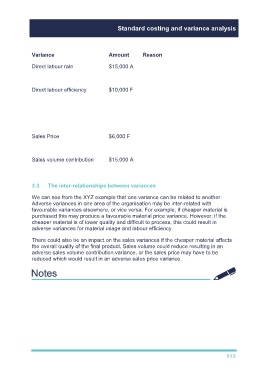

Variance Amount Reason

Direct labour rate $15,000 A Standard rate set too low

Higher pay rises

Direct labour efficiency $10,000 F Standard hours set too high

More skilled workers

Higher grade of material

More efficient working

Sales Price $6,000 F Higher quality product

Higher selling price

Sales volume contribution $15,000 A Quality control problems

Lower sales volume

3.3 The inter-relationships between variances

We can see from the XYZ example that one variance can be related to another.

Adverse variances in one area of the organisation may be inter-related with

favourable variances elsewhere, or vice versa. For example, if cheaper material is

purchased this may produce a favourable material price variance. However, if the

cheaper material is of lower quality and difficult to process, this could result in

adverse variances for material usage and labour efficiency.

There could also be an impact on the sales variances if the cheaper material affects

the overall quality of the final product. Sales volume could reduce resulting in an

adverse sales volume contribution variance, or the sales price may have to be

reduced which would result in an adverse sales price variance.

TYU 9

113