Page 393 - SBR Integrated Workbook STUDENT S18-J19

P. 393

UK GAAP

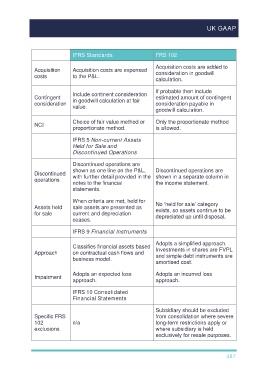

IFRS Standards FRS 102

Acquisition costs are added to

Acquisition Acquisition costs are expensed consideration in goodwill

costs to the P&L.

calculation.

If probable then include

Include continent consideration

Contingent in goodwill calculation at fair estimated amount of contingent

consideration consideration payable in

value.

goodwill calculation.

Choice of fair value method or Only the proportionate method

NCI

proportionate method. is allowed.

IFRS 5 Non-current Assets

Held for Sale and

Discontinued Operations

Discontinued operations are

shown as one line on the P&L, Discontinued operations are

Discontinued with further detail provided in the shown in a separate column in

operations

notes to the financial the income statement.

statements.

When criteria are met, held for

Assets held sale assets are presented as No ‘held for sale’ category

exists, so assets continue to be

for sale current and depreciation depreciated up until disposal.

ceases.

IFRS 9 Financial Instruments

Adopts a simplified approach.

Classifies financial assets based

Approach on contractual cash flows and Investments in shares are FVPL

and simple debt instruments are

business model.

amortised cost.

Adopts an expected loss Adopts an incurred loss

Impairment

approach. approach.

IFRS 10 Consolidated

Financial Statements

Subsidiary should be excluded

Specific FRS from consolidation where severe

102 n/a long-term restrictions apply or

exclusions where subsidiary is held

exclusively for resale purposes.

387