Page 439 - SBR Integrated Workbook STUDENT S18-J19

P. 439

Answers

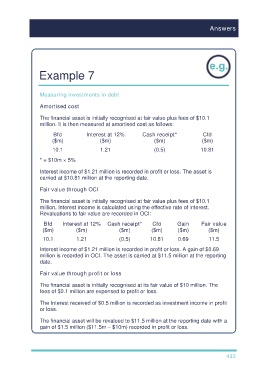

Example 7

Measuring investments in debt

Amortised cost

The financial asset is initially recognised at fair value plus fees of $10.1

million. It is then measured at amortised cost as follows:

Bfd Interest at 12% Cash receipt* Cfd

($m) ($m) ($m) ($m)

10.1 1.21 (0.5) 10.81

* = $10m × 5%

Interest income of $1.21 million is recorded in profit or loss. The asset is

carried at $10.81 million at the reporting date.

Fair value through OCI

The financial asset is initially recognised at fair value plus fees of $10.1

million. Interest income is calculated using the effective rate of interest.

Revaluations to fair value are recorded in OCI:

Bfd Interest at 12% Cash receipt* Cfd Gain Fair value

($m) ($m) ($m) ($m) ($m) ($m)

10.1 1.21 (0.5) 10.81 0.69 11.5

Interest income of $1.21 million is recorded in profit or loss. A gain of $0.69

million is recorded in OCI. The asset is carried at $11.5 million at the reporting

date.

Fair value through profit or loss

The financial asset is initially recognised at its fair value of $10 million. The

fees of $0.1 million are expensed to profit or loss.

The Interest received of $0.5 million is recorded as investment income in profit

or loss.

The financial asset will be revalued to $11.5 million at the reporting date with a

gain of $1.5 million ($11.5m – $10m) recorded in profit or loss.

433