Page 458 - SBR Integrated Workbook STUDENT S18-J19

P. 458

Chapter 25

Example 1 – continued

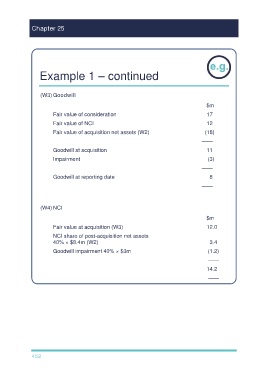

(W3) Goodwill

$m

Fair value of consideration 17

Fair value of NCI 12

Fair value of acquisition net assets (W2) (18)

——

Goodwill at acquisition 11

Impairment (3)

——

Goodwill at reporting date 8

——

(W4) NCI

$m

Fair value at acquisition (W3) 12.0

NCI share of post-acquisition net assets

40% × $8.4m (W2) 3.4

Goodwill impairment 40% × $3m (1.2)

——

14.2

——

452