Page 462 - SBR Integrated Workbook STUDENT S18-J19

P. 462

Chapter 25

Example 2 – continued

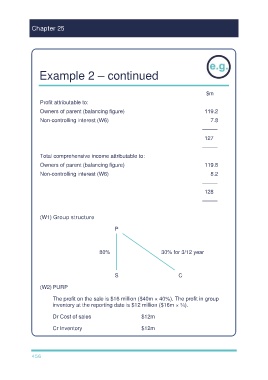

$m

Profit attributable to:

Owners of parent (balancing figure) 119.2

Non-controlling interest (W6) 7.8

–––––

127

–––––

Total comprehensive income attributable to:

Owners of parent (balancing figure) 119.8

Non-controlling interest (W6) 8.2

–––––

128

–––––

(W1) Group structure

P

80% 30% for 3/12 year

S C

(W2) PURP

The profit on the sale is $16 million ($40m × 40%). The profit in group

inventory at the reporting date is $12 million ($16m × ¾).

Dr Cost of sales $12m

Cr Inventory $12m

456