Page 487 - SBR Integrated Workbook STUDENT S18-J19

P. 487

Answers

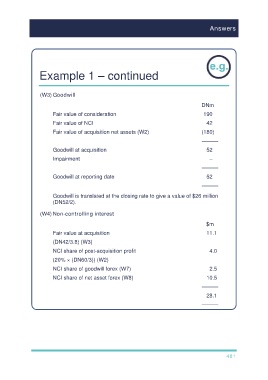

Example 1 – continued

(W3) Goodwill

DNm

Fair value of consideration 190

Fair value of NCI 42

Fair value of acquisition net assets (W2) (180)

———

Goodwill at acquisition 52

Impairment –

———

Goodwill at reporting date 52

———

Goodwill is translated at the closing rate to give a value of $26 million

(DN52/2).

(W4) Non-controlling interest

$m

Fair value at acquisition 11.1

(DN42/3.8) (W3)

NCI share of post-acquisition profit 4.0

(20% × (DN60/3)) (W2)

NCI share of goodwill forex (W7) 2.5

NCI share of net asset forex (W8) 10.5

———

28.1

———

481