Page 8 - PowerPoint Presentation

P. 8

COST VOLUME PROFIT ANALYSIS

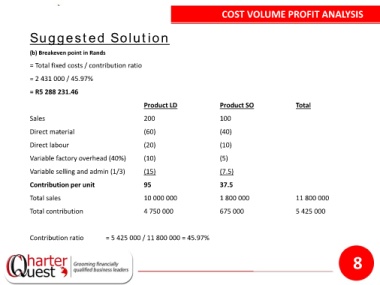

Suggested Solution

(b) Breakeven point in Rands

= Total fixed costs / contribution ratio

= 2 431 000 / 45.97%

= R5 288 231.46

Product LD Product SO Total

Sales 200 100

Direct material (60) (40)

Direct labour (20) (10)

Variable factory overhead (40%) (10) (5)

Variable selling and admin (1/3) (15) (7.5)

Contribution per unit 95 37.5

Total sales 10 000 000 1 800 000 11 800 000

Total contribution 4 750 000 675 000 5 425 000

Contribution ratio = 5 425 000 / 11 800 000 = 45.97%

8