Page 26 - P6 Slide Taxation - Lecture Day 3 - VAT Part 2

P. 26

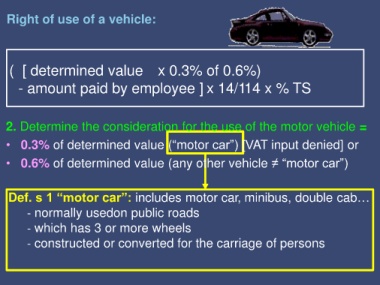

Right of use of a vehicle:

( [ determined value x 0.3% of 0.6%)

- amount paid by employee ] x 14/114 x % TS

2. Determine the consideration for the use of the motor vehicle =

• 0.3% of determined value (“motor car”) [VAT input denied] or

• 0.6% of determined value (any other vehicle ≠ “motor car”)

Def. s 1 “motor car”: includes motor car, minibus, double cab…

- normally usedon public roads

- which has 3 or more wheels

- constructed or converted for the carriage of persons