Page 24 - P6 Slide Taxation - Lecture Day 3 - VAT Part 2

P. 24

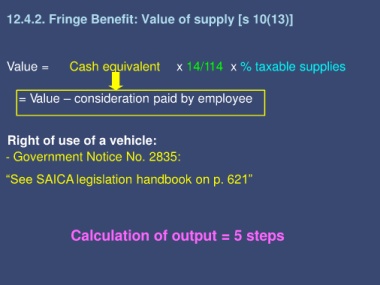

12.4.2. Fringe Benefit: Value of supply [s 10(13)]

Value = Cash equivalent x 14/114 x % taxable supplies

= Value – consideration paid by employee

Right of use of a vehicle:

- Government Notice No. 2835:

“See SAICA legislation handbook on p. 621”

Calculation of output = 5 steps