Page 21 - P6 Slide Taxation - Lecture Day 3 - VAT Part 2

P. 21

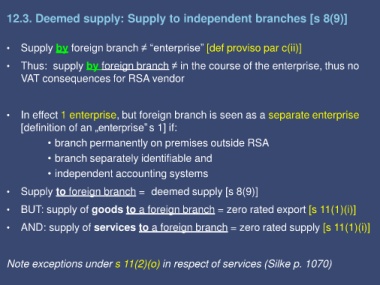

12.3. Deemed supply: Supply to independent branches [s 8(9)]

• Supply by foreign branch ≠ “enterprise” [def proviso par c(ii)]

• Thus: supply by foreign branch ≠ in the course of the enterprise, thus no

VAT consequences for RSA vendor

• In effect 1 enterprise, but foreign branch is seen as a separate enterprise

[definition of an „enterprise‟s 1] if:

• branch permanently on premises outside RSA

• branch separately identifiable and

• independent accounting systems

• Supply to foreign branch = deemed supply [s 8(9)]

• BUT: supply of goods to a foreign branch = zero rated export [s 11(1)(i)]

• AND: supply of services to a foreign branch = zero rated supply [s 11(1)(i)]

Note exceptions under s 11(2)(o) in respect of services (Silke p. 1070)