Page 258 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 258

Chapter 10

6.3 The Capital Asset Pricing Model (CAPM)

The CAPM enables us to calculate the required return from an

investment given the level of risk associated with the investment

(measured by its beta factor).

Before showing how the CAPM formula can be used to derive a suitable

risk adjusted cost of capital for discounting, we first need to introduce

the model and explain the terminology surrounding it.

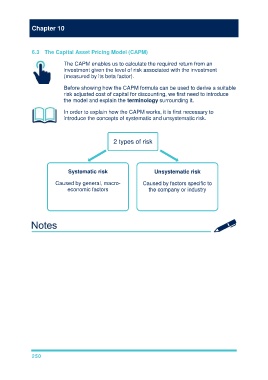

In order to explain how the CAPM works, it is first necessary to

introduce the concepts of systematic and unsystematic risk.

2 types of risk

Systematic risk Unsystematic risk

Caused by general, macro- Caused by factors specific to

economic factors the company or industry

(e.g. recession, interest rates, (e.g. systems failure, R+D

exchange rates) success. strikes)

250