Page 211 - Microsoft Word - 00 Prelims.docx

P. 211

Capital and financing

Fixed v floating charges

Characteristics

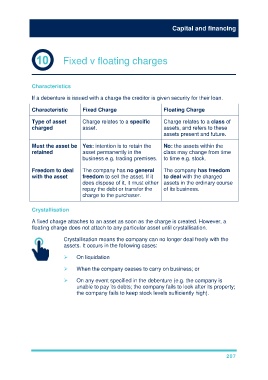

If a debenture is issued with a charge the creditor is given security for their loan.

Characteristic Fixed Charge Floating Charge

Type of asset Charge relates to a specific Charge relates to a class of

charged asset. assets, and refers to these

assets present and future.

Must the asset be Yes: intention is to retain the No: the assets within the

retained asset permanently in the class may change from time

business e.g. trading premises. to time e.g. stock.

Freedom to deal The company has no general The company has freedom

with the asset freedom to sell the asset. If it to deal with the charged

does dispose of it, it must either assets in the ordinary course

repay the debt or transfer the of its business.

charge to the purchaser.

Crystallisation

A fixed charge attaches to an asset as soon as the charge is created. However, a

floating charge does not attach to any particular asset until crystallisation.

Crystallisation means the company can no longer deal freely with the

assets. It occurs in the following cases:

On liquidation

When the company ceases to carry on business; or

On any event specified in the debenture (e.g. the company is

unable to pay its debts; the company fails to look after its property;

the company fails to keep stock levels sufficiently high).

207